Navigating the new climate reporting obligations – what businesses need to know

On 9 September 2024, amendments were made to the Corporations Act 2001 (Cth) introducing new climate reporting obligations for specific entities. The reporting obligations will have a staged implementation from 1 January 2025. This new regime will have significant impacts for businesses required to report, and other businesses within their supply chains may also find their contractual reporting obligations increasing as a result.

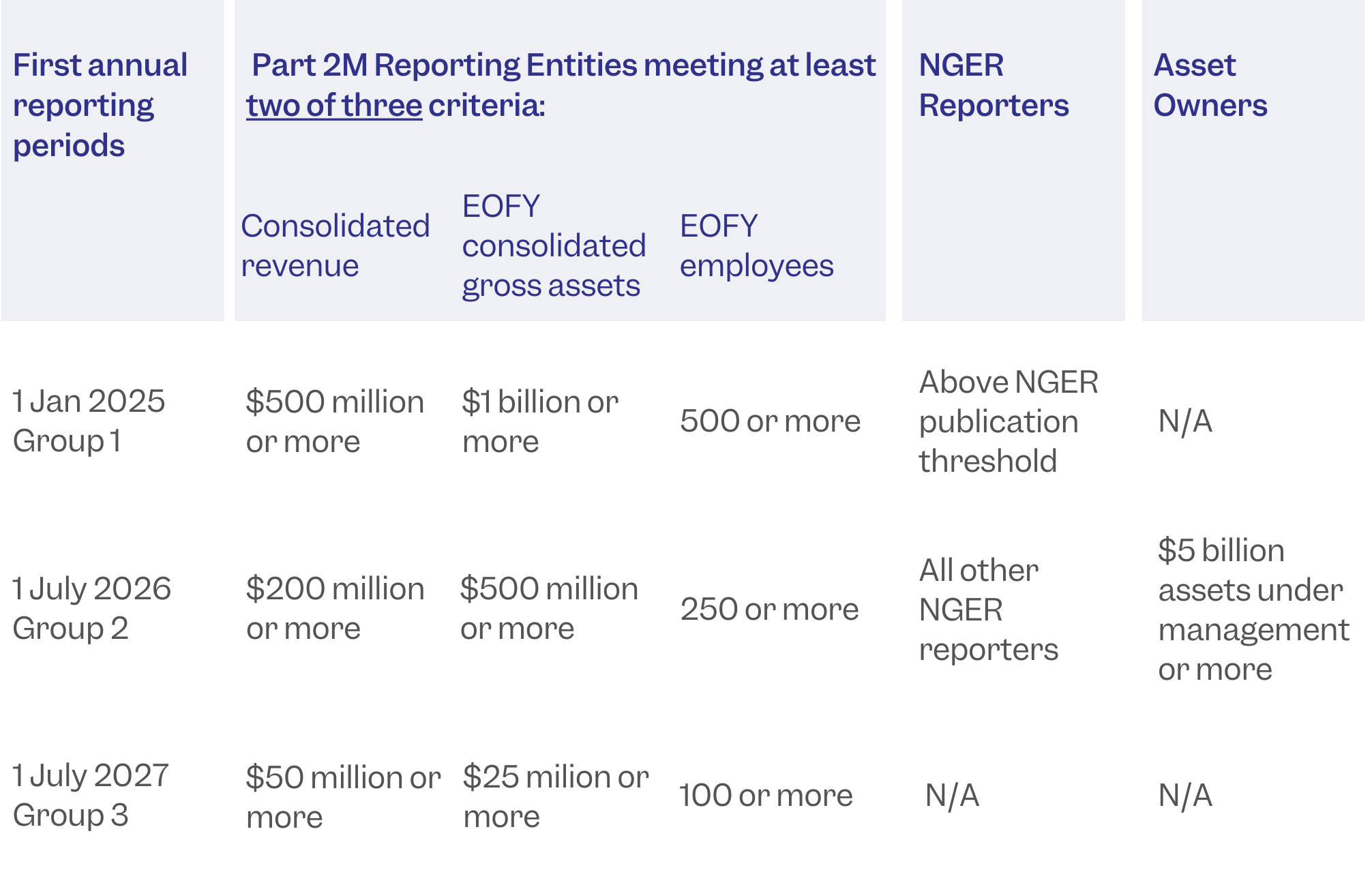

Who is captured and when does reporting start?

The entities required to report are split into three groups as set out in the table below, with Group 1 commencing reporting for their first usual reporting period commencing after 1 January 2025 (i.e., for businesses reporting in financial years, from 1 July 2025 to 30 June 2026).

Relevantly, the new regime will apply to not-for-profits, but registered charities are excluded. Group 3 captures “large proprietary companies”, and so small proprietary companies and other businesses that do not meet the Group 1, 2 or 3 criteria will not be captured.

What is required to be reported?

The new legislation requires certain entities to disclose information related to climate governance, risk and strategy, including greenhouse gas emissions and targets (scopes 1 to 3), and an assessment of the entity's resilience to climate-related changes using scenario analysis.

These disclosures will form part of a new sustainability report which falls within the existing annual reporting framework.

Details about the disclosures to be made are found in AASB S2, which is part of the Australian Sustainability Reporting Standards prepared by the AASB. The sustainability report must be audited, although the auditing assurance standards are still being finalised.

Importantly:

- businesses are only required to use all reasonable information available to them in preparing the report, provided it can be obtained without undue cost or effort;

- data can be used from a different reporting period, provided certain criteria is met;

- commercially sensitive information can be excluded from reporting, provided that to include it would "prejudice seriously" the economic benefits, and it is impossible for the entity to disclose the information in some other way;

- scope 3 emissions only need to be reported from an entity’s second year of reporting; and

- Group 3 entities are only required to prepare a sustainability report if the business faces material climate related risks or opportunities.

Other limitations in place to assist with the transition include:

- the directors declaration to be included with the sustainability report will only need to refer to the entity having taken “reasonable steps” to comply with the requirements up until 1 January 2028, when the declaration will then need to be to the effect that the entity has complied with the reporting requirements;

- a limited liability regime in relation to private litigants, whereby private litigants will not be able to take action against entities:

- up until 31 December 2025, in respect of representations as to future matters in sustainability reports; and

- up until 31 December 2027, in respect of disclosures made in sustainability reports about scope 3 emissions, the scenario analysis, or the entity’s transition plans; and

- in respect of the audit, there will be a gradual increase in the assurance level required over the first few years of an entity reporting.

Penalties and enforcement

As the regime forms a part of the Corporations Act, the usual provisions in relation to matters such as directors duties, misleading and deceptive conduct and exercising reasonable care in preparing reports apply.

In addition, the regime introduces a number of new penalties for failure to comply with the regime, including that ASIC can issue a notice to a company where it considers a business has not complied with the sustainability report requirements, and direct that the company rectify its report.

ASIC has indicated that it will take a pragmatic and proportionate approach to enforcement of the new regime as businesses adjust.

How to prepare?

Businesses captured by the new regime should be acting now to ensure they are prepared for their first reporting period.

In carrying out this preparation, businesses might consider:

- the climate competency of its board and management, and whether additional support is required;

- establishing a dedicated team to oversee compliance, ensuring roles encompass sustainability, finance and risk management;

- the data and systems needed to capture the required information for disclosure, including whether contracts with third parties should be amended so information can be sought from those parties to assist with scope 3 reporting.

For businesses that are not captured by the new regime, it may be prudent to identify any businesses they deal with which are likely to be captured by the regime, and to understand whether those larger businesses will want to obtain information from them for use in preparing their sustainability report. Businesses not captured by the regime could use this time now to understand and if necessary, negotiate, the extent of information they will provide. Similarly, any new amended contracts with reporting entities should be carefully scrutinised in relation to obligations to provide information, to ensure that any such obligations will not be too onerous on the company producing the information.

Conclusion

The introduction of mandatory climate reporting is not just a compliance obligation, it represents an opportunity for organisations to demonstrate their resilience and commitment to sustainability. By embracing these changes, businesses can enhance their strategic position and contribute positively to the broader goal of climate accountability.

This article provides general commentary only. It is not legal advice. Before acting on the basis of any material contained in this article, seek professional advice.

Our ESG and sustainability expertise

Our team works closely with clients to identify and develop ways to integrate ESG-related solutions into business as usual, with the goal of benefitting clients, their shareholders as well as the communities they operate in. We want to ensure you not only legally comply with ESG requirements, but also strengthen your position in the market.

Find out more about how our ESG and sustainability experts can support your business on it's journey to sustainability.

Related Insights

Regulator focus locks onto greenwashing

ESG update: changes to sustainability reporting standards and regulators continue to take action

Compliance and Beyond - ESG and Unfair Contract Terms

DMAW Lawyers launches ESG committee